Bank Capital Doesn't Exist

Not outside of a balance sheet, anyway.

Thanks to a successful Wall Street pushback against regulators, the ever-controversial topic of bank capital has been in the news again.

As a quick reminder, the main reason that bank capital rules are contentious is:

Higher bank capital ratios are generally better for society, resulting in safer banks and preventing 2008-style disasters.1

But higher bank capital ratios are generally worse for bank owners & executives, resulting in higher funding costs and lower profits.

Here’s the thing about bank capital: if you have the wrong mental model for how banking works, bank capital is intuitive and easily ‘understood’ in an inaccurate way.

But if you have the right mental model for how banking works, bank capital becomes less intuitive and more complex - but also far more accurate.

Today, I want to take a quick look at what bank capital is, what it isn’t, why it matters, and how misunderstandings lead to misinformed policy prescriptions.

Two models of banking

#1: The wrong model

Here’s a super simplified model that reflects the widely accepted understanding of how banking works:

Banks can raise money in two different ways:

Deposits (low-cost debt funding from depositors)

Capital (high-cost equity funding from shareholders)

Banks do one of three things with this money:

Hold it in cash

Use it to fund low-risk assets like Treasury bonds

Use it to fund high-risk assets like loans to individuals & businesses

Under this model, banks first raise money via deposits & capital and then use that money in different ways - like holding it in cash, using it to buy bonds, or lending it out.

Here, bank capital has a natural and intuitive meaning - it’s just the pool of money that the bank raises from shareholders. Critically, that pool is entirely separate from the pool marked deposits.

Next time you’re reading an article on bank capital, keep an eye out for phrasing indicating that banks ‘hold’ capital. The idea that capital is something that banks have or hold is a pernicious misconception stemming from model #1.

Sorry, Investopedia, but all three of these sentences are wrong.

#2: The right model

Here’s a super simplified model that reflects how banking actually works in practice:

Banks don’t need to raise money at all.

When a bank wants to fund an asset, it just creates new deposits.

The idea that banks don’t actually need to raise money in order to fund their assets sounds crazy, but this model is more accurate than you might think.2

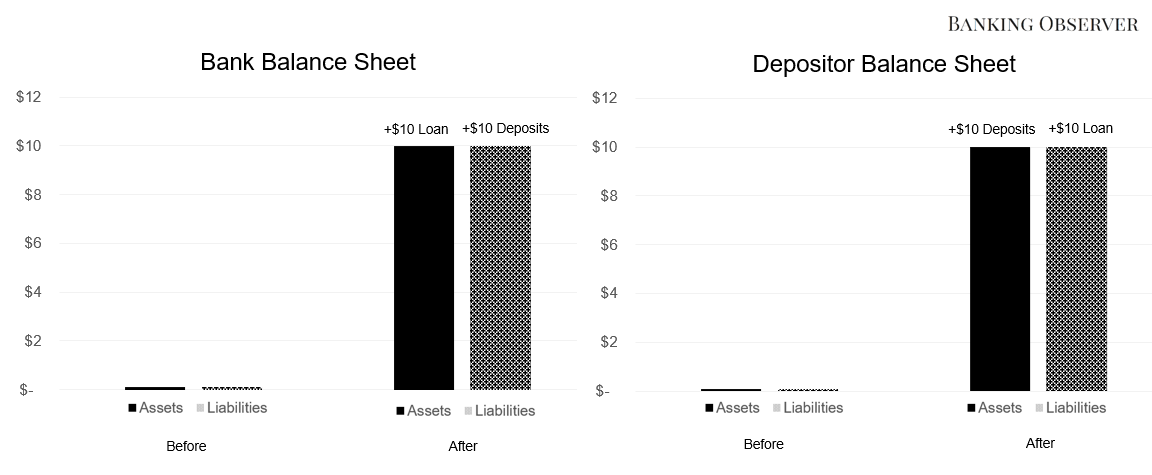

If a bank wants to fund a new loan, it just needs to mark up the value of the borrower’s deposit account while adding the loan as an asset to its balance sheet. The bank can do a similar accounting operation if it wants to purchase a Treasury bond from one of its depositors.

Here’s the basic loan creation balance sheet transaction:

Still, there are a few reasons that a bank might want to raise non-deposit funding (capital) under this model too, even if that funding is more expensive:

If a depositor wants to withdraw some of their deposits, the bank will need some cash on hand to honor the request. One way for a bank to get that cash is by raising capital, which involves selling equity to shareholders in exchange for cash.3

Without equity funding, if the bank’s assets decline in value, it’ll be insolvent immediately (the bank will owe depositors more than what the bank owns). There’s no buffer.

So, let’s assume the bank raises a bit of capital before funding assets. Here’s what the balance sheet transaction looks like now:

Under this model, bank capital doesn’t refer to any particular asset. In fact, capital isn’t even on the asset side of the balance sheet.

Instead, bank capital is nothing more than the gap that exists between assets and liabilities as a result of a bank raising non-deposit funding.

Let’s note a few quick things about the concept of bank capital under this new model when compared to the first:

A bank doesn’t raise capital in order to fund assets. Instead, capital is used as a risk management tool (both in terms of liquidity & solvency).

There’s no such thing as a ‘choice’ between capital and deposits when it comes to asset funding. Funding is inextricably linked to deposit creation.

Capital isn’t a pool of money that the bank can ‘hold'.’ Yes, a bank can hold the cash associated with the initial capital raising, but the bank’s capital doesn’t disappear if the cash flows out of the bank.

This third point is why I say that bank capital ‘doesn’t exist’ - because under the right model of banking, we can see that bank capital doesn’t refer to any particular asset or pool of money. Instead, bank capital is purely an accounting phenomenon - the excess of assets over liabilities.

Why does any of this matter?

This all might seem like an unnecessarily nuanced analysis. Does it really matter if we understand capital as a specific pool of money or as an accounting phenomenon?

I think it does. The most serious problem of operating under model #1 is thinking that you can connect changes in bank capital levels to the performance of specific assets (that is, those assets that were funded with capital, not deposits).

This misunderstanding manifests in a number of ways, including:

Advocating for policies that call for banks to separately fund risky assets with capital and safe assets with deposits.

Not understanding that a markdown in the value of any asset will impact bank capital levels, not just those assets that were “funded” with capital.

Misinterpreting risk-weighted capital metrics (an extremely important part of capital regulation that I’ll discuss in a separate article) as indicating which specific assets need to be backed by capital rather than as a tool to proportionally scale an entire balance sheet.

Enlightened minds can disagree on what the right rules are for bank capital regulation. But we shouldn’t disagree on what bank capital is in the first place.

Well, up to a point. Higher bank capital ratios also result in reduced lending activity, so there’s a tradeoff between safety and considerations of economic growth, loan accessibility, homeownership rates, etc.

The most important missing component of this model (and this section as a whole) is the presence of other banks. If Bank 1 wants to purchase an asset from a depositor who only has an account at Bank 2, for instance, Bank 1 might need to raise capital in the first place to have the reserves needed to settle the transaction. Similarly, if a depositor at Bank 1 wants to transfer money to Bank 2, Bank 1 will also need reserves.

Ultimately, I don’t discuss this because it adds more complexity than is needed to understand bank capital. Moreover, in the first instance (asset purchase), Bank 2 still needs to create new deposits to settle the transaction - deposit creation is inextricably linked with asset funding. The second instance (transfer), meanwhile, is best understood as a special case of cash withdrawal, which I do discuss.