Explaining the role of the dollar as the global reserve currency

We explore the outsize role of the dollar in global finance and what it means to be a reserve currency.

Much like a shared language is necessary to communicate complex thoughts, a shared currency is necessary to execute complex transactions. Without money, a farmer selling wheat and a cobbler selling shoes will only be able to trade if the former wants shoes and the latter wants wheat. Economists refer to this as the ‘coincidence of wants’ problem, and it provides a compelling reason for why societies tend to gravitate towards using a common currency as a medium of exchange. It’s far better for buyers and sellers to intermediate their transactions with money than to hope for a mutually agreeable barter. While the international trade system is a bit more complex than a barter economy, it is the same underlying coincidence of wants problem that renders a reserve currency necessary.

Just like a common currency facilitates trade within borders, a reserve currency facilitates trade between them. Suppose that Brazil wants to buy some goods from Mexico. Brazil could try and pay for the goods with reals, the Brazilian currency, but Mexico is unlikely to accept. Reals can only be used to buy things from Brazil, which limits Mexico’s trading options. Brazil is unlikely to have any pesos, the Mexican currency, because pesos would have been similarly unappealing to Brazil in the past. Since each country’s currency is unattractive to the other, Brazil and Mexico face a coincidence of wants problem that can be solved by introducing a new medium of exchange. This medium is the reserve currency, a third currency which can be used to conduct trade around the globe.

In the recent past, this role has been filled by the US dollar. According to the Federal Reserve, America’s central bank, the dollar is used for more than 70% of cross-border transactions in most areas of the world. Europe is an exception, with the majority of trade conducted in euros, owing to the unique situation of a block of disparate countries using a single currency. The network effects that drive currency adoption mean that countries are willing to accept dollars because they know that other countries will accept dollars. Additionally, the dollar has a number of advantages as a reserve currency that competitors have been unable to match.

First, the Fed’s credibility in controlling inflation makes the dollar seem like a predictable store of value. Even in the midst of current decades-high inflation, few analysts expect the Fed to allow high inflation to continue over the next several years. Second, America is the world’s largest import market, with a consistent trade deficit since 1976. This means dollars persistently flow out of the country to exporters, leaving those countries flush with dollars. Structurally, foreign holdings of dollars are going to be large, making the dollar a ‘natural’ reserve currency.

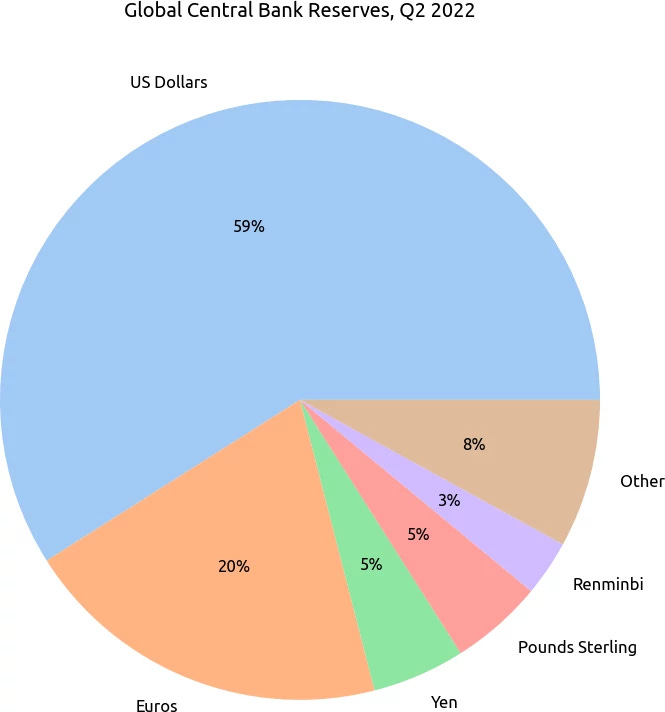

Finally, and most importantly, the dollar offers access to the deepest and most liquid financial markets in the world. Countries that trade in dollars end up with huge volumes of the currency, either due to pending imports or settled exports. At the national scale, sticking those dollars in a bank account is not an option. According to the Congressional Research Service, a government think tank, dollars represent about 60% of total global central bank reserves. American financial markets, and the Treasury market in particular, are some of the few global markets that can accommodate such a huge amount of money. The fragmentation of European markets, with no supranational treasury, has been an albatross hanging around the neck of the euro as it has grown in importance as a global currency. Capital controls in China have resulted in similar difficulties for the renminbi.

The dollar’s status as the world’s reserve currency has largely benefited America. The increased demand for Treasuries lowers the interest rate the American government has to pay on its debt. Further, the government can weaponize the dollar by using sanctions to further foreign policy objectives. In 2022, America sanctioned over 400 Russian entities in response to the Russian invasion of Ukraine, effectively cutting off their access to the Western financial system.

Domestic critics of the dollar serving as the global reserve currency argue that increased demand for the dollar limits American manufacturing competitiveness. Since a strong dollar makes foreign imports cheaper, there are likely fewer manufacturing jobs in the country than there otherwise would be. However, this is unlikely to lead to job losses in absolute terms, since the makeup of consumption would simply shift toward services. Moreover, a strong dollar means that production costs are lower for companies that rely on foreign inputs.

The benefits that accrue to America are not without certain costs to the rest of the world. The dollar’s status means that American monetary policy tends to get exported. When the Fed raises interest rates, investors allocate more capital to America, causing the dollar to strengthen. For a foreign country, this will make importing goods denominated in dollars more expensive in terms of the local currency, even if the underlying supply and demand has not changed. To sterilize this effect, the central bank of the foreign country will likely have to raise interest rates as well, even if such contractionary monetary policy is not appropriate.

Prior to the Bretton Woods Conference of 1944, which cemented the future of the dollar as the global reserve currency, the role was played by the pound sterling. Two world wars, though, left Britain with a battered economy. With the British share of imports as a portion of global trade falling, foreign countries were unable to get their hands on enough pounds to use the currency to trade. Additionally, Europe had been drained of its gold reserves, rendering Britain unable to guarantee the stability of the gold standard. With the future of the dollar’s reserve status a matter of debate, this transition is instructive for what it would take to dethrone the dollar. As long as America remains the world’s largest importer, and as long as investors perceive the Fed to be committed to stable monetary policy, the dollar is likely to retain its crown for years to come.