Fed issues third-straight rate hike, refuses to rule out recession

The risk of a severe contraction has grown, but it is not guaranteed.

On Wednesday, the Federal Reserve, America’s central bank, elected to raise interest rates by 0.75% in its third straight interest rate hike. This decision brings the Fed’s target interest rate to between 3 and 3.25%, a level last seen during the economic boom that preceded the Global Financial Crisis. In language reminiscent of his recent hawkish speech at Jackson Hole, Fed chair Jerome Powell said that “reducing inflation is likely to require a sustained period of below trend growth”, and acknowledged that a recession was not off the table. Using the Fed’s preferred inflation measure, prices are increasing at more than double the central bank’s 2% target, despite the most aggressive monetary tightening in decades.

Powell’s tough talk is designed to convey the Fed’s willingness to create economic pain in order to bring inflation down, something that has stopped many central banks from continuing their own contractionary policy in the past. Yet severe economic consequences of the type expected by most market participants are far from guaranteed. While a serious recession remains a risk, there are encouraging markers of resilience in the American economy. Gross domestic income, an alternative measure of national output that is theoretically equal to gross domestic production, has risen in real terms this year, even as its more famous counterpart has fallen. Real consumer spending also continues to rise, which is no small feat given such high inflation figures.

Given these strengths, it remains an open question whether a recession will actually materialize. One possibility is that changes in the global economic landscape are causing a transition to a permanently higher price level. In an increasingly fractured world fraught with geopolitical tension, the halcyon days of free-wheeling globalization are over. While full scale “deglobalization” will not occur, many businesses are increasing domestic production and diversifying their international supply chains, both of which force them to increase final prices. Political forces are encouraging the reshoring of critical industries. Look to the recent CHIPS act in America, a rare bipartisan effort which authorized billions of dollars in semiconductor manufacturing subsidies.

Permanent changes to supply chains certainly explain persistent price pressures far better than the more popular narrative that supply chain issues are due to temporary pandemic-related disruptions. But if these changes, along with idiosyncratic increases in energy prices, are the cause of inflation, it is likely that inflation can be brought under control without a severe contraction. Interest rate increases should bring demand back in line with supply, but this demand reduction will not necessarily feed through to layoffs and a decline in business investment. The supply chain adjustments described will actually require more domestic hiring and investment, which sterilizes two of the common contributors to serious downturns.

On paper, growth would decline as the economy transitions to a world that looks like a high-tech version of the time before China joined the World Trade Organization. Curiously, this implies that a recession could occur without the typical accompanying spike in unemployment. The current strength of the American labor market certainly makes this a credible outcome. Despite investor sentiment being as poor as it was during the Global Financial Crisis, a mild recession paired with very little rise in the unemployment rate remains a likely possibility.

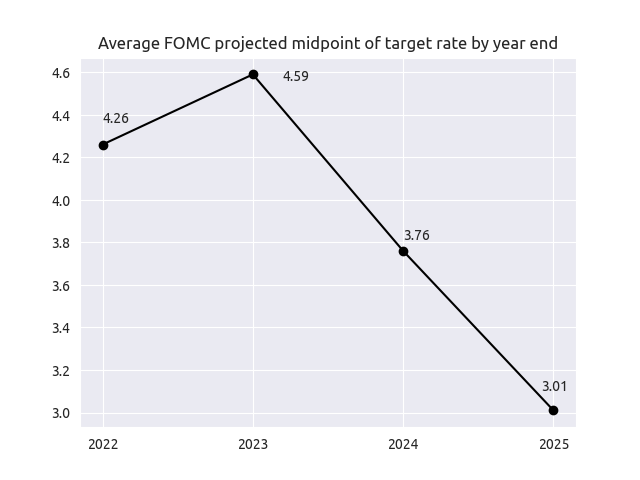

Along with the interest rate decision, the Fed also released its dot-plot, which is used to signal the likely path of future interest rates. Markets fretted over the fact that the Fed’s policy makers see rates rising to more than 4.5% in 2023. Yet in the Fed’s dot-plot released this time last year, not a single policy maker saw rates eclipsing 0.75% in 2022. Future rates will depend heavily on the length and magnitude of the coming economic consequences of current rates. Investors should take note that, for better or for worse, the Fed of today rarely knows what the Fed of tomorrow will do.