In Praise of Fiscal Irresponsibility

Let's stop treating the deficit like a serious issue.

Recently, The Economist ran an article lamenting the fact that America’s budget deficit has become an afterthought for both voters and policymakers. In the run-up to the 2024 presidential election, the deficit seems to have all but disappeared as a serious policy issue.

The Economist’s view on the deficit is a natural and intuitive one. Under this view, sustained deficits are a sign of fiscal irresponsibility and profligacy. Because deficits occur when the federal government lives beyond its means, they must inevitably lead to disaster, just as they would for any other economic actor.

This view is wrong. In reality, the government isn’t just like any other economic actor. As a result, sustained government deficits aren’t necessarily a sign of looming danger.

Today, I want to explore why this is and understand the factors that truly matter when it comes to fiscal policy.

What is a deficit, anyway?

A quick reminder on what the federal deficit is:

The US government takes in money through taxes. The big three sources of federal revenue are individual income taxes, Social Security & Medicare taxes, and corporate income taxes.

The US government also has expenses, such as spending on Social Security, healthcare, education, transportation, and interest on borrowing.

When expenses are higher than taxes, a deficit occurs - the money flowing out is greater than the money flowing in.

Large, sustained deficits are now a fact of life in modern American politics. The last time the budget was in surplus was in 2001. For the government’s 2023 fiscal year, the deficit amounted to $1.7 trillion, equivalent to about 27% of federal expenses.

To bridge the gap between taxes and expenses, the government borrows money in the form of Treasury notes, bills, and bonds.

For almost any other economic actor, consistently spending more than they take in and making up the difference through borrowing would be a disaster. So, why is the government any different?

The federal government is a currency issuer

Households, businesses, and state/county/local governments need to care about budget deficits for one reason: for all these parties, dollars are a limited resource.

This is such an obvious point that it feels absurd to state. After all, if you want to spend money, it needs to come from somewhere. Money doesn’t grow on trees - right?

Not quite. There is one party for whom this budget constraint doesn’t apply: the federal government. In fact, because the government is a currency issuer that has the exclusive legal right to make new dollars, dollars are an unlimited resource for them.

If the federal government wants to spend money, the dollars don’t need to ‘come from somewhere’. For the government, dollars are nothing more than digital entries on a spreadsheet that can be marked up or down at will.

You and I can run out of dollars. But by virtue of being a currency issuer, the federal government cannot.

And isn’t it a little odd to care about a ‘deficit’ of something that can never actually run out?1

But what about inflation?

In my experience, most people’s initial reaction to the idea of the federal government as a currency issuer is to ask about inflation.

After all, the government can’t literally create new dollars to pay its bills without limit. That would risk severely devaluing the very same dollars being created.

Inflation does pose a serious constraint on how many dollars the government can create (or, more accurately, how many dollars they can spend). But this is exactly my point. The deficit is an entirely artificial constraint, in stark contrast to the very real threat of inflation.

Can a government deficit fuel the risk of inflation? Absolutely - but the scale of that risk depends on a bunch of factors, including:

How the deficit is financed,

how deficit spending is actually used,

and what kind of economic environment that deficit spending takes place in.

A simple one-to-one relationship between deficits and inflation, however, does not exist.

In the US, the federal government has run budget deficits of varying size and scale nearly every year between 2000 and 2020. And yet, in that timeframe, the average monthly inflation reading (as measured by CPI) was just 2.1%.

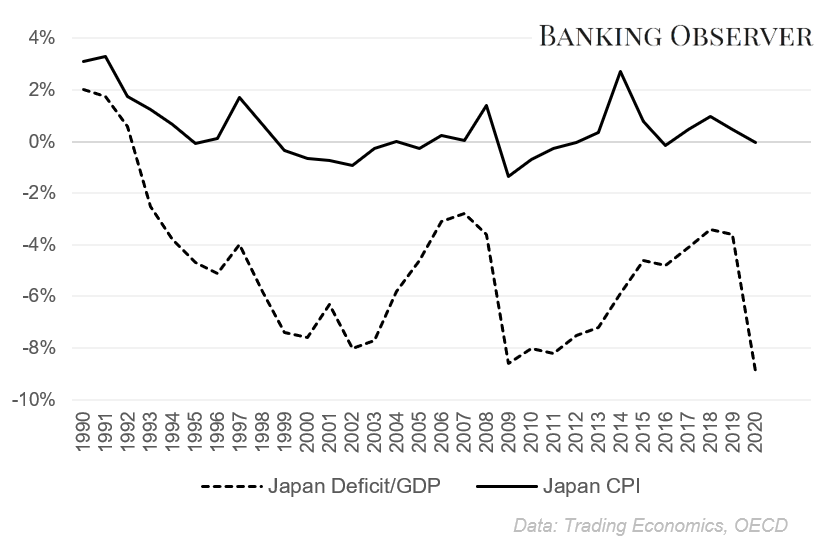

Japan provides an even more instructive example. Since 1990, Japan has run significant budget deficits in an attempt to stimulate the economy and stoke inflation. But during that time, deflation still occurred in some years, and it took the global post-Covid inflation shock for Japan to see sustained price increases.

Data: Trading Economics, OECD

Addressing other concerns

Two brief(ish) points on other concerns related to the deficit.

1. Debt

Under the current regime, deficits naturally lead to increases in the national debt. For debt hawks, this makes sustained deficits unconscionable.

A full treatment of the national debt and its many (many) misinterpretations is outside the scope of this article. But I’ll note a few quick reasons that the deficits → debt → disaster argument against deficits doesn’t hold water:

America’s substantial national debt is, in many ways, a good thing. Treasuries allow for a default-free store of wealth for citizens, increase the efficiency of financial markets, and promote the role of the dollar as the global reserve currency.

The fact that deficits inevitably lead to increases in the national debt is a policy choice. You could print money (create reserves) to pay for deficit spending (paying interest on reserves makes these two options more similar than they appear, though).

Since the federal government is a currency issuer, the US will never be forced to default on its debt, no matter how large (barring silly political constraints like the debt ceiling). Japan, for instance, has been able to sustain extraordinarily high government debt for decades. As with deficits, the true constraint is inflation.

2. Crowding out

This is a slightly more technical point. You can skip to the conclusion without loss.

Deficits are often blamed for crowding out private investment and leading to slower economic growth. The model here is:

The government deficit increases.

To finance the deficit, the government needs to borrow more by issuing bonds.

These bonds compete with other opportunities for the same pool of investor money.

Increased competition for investor money leads to higher interest rates.

Higher rates make it more expensive for companies to finance new investments or for individuals to finance new purchases, both leading to lower growth.

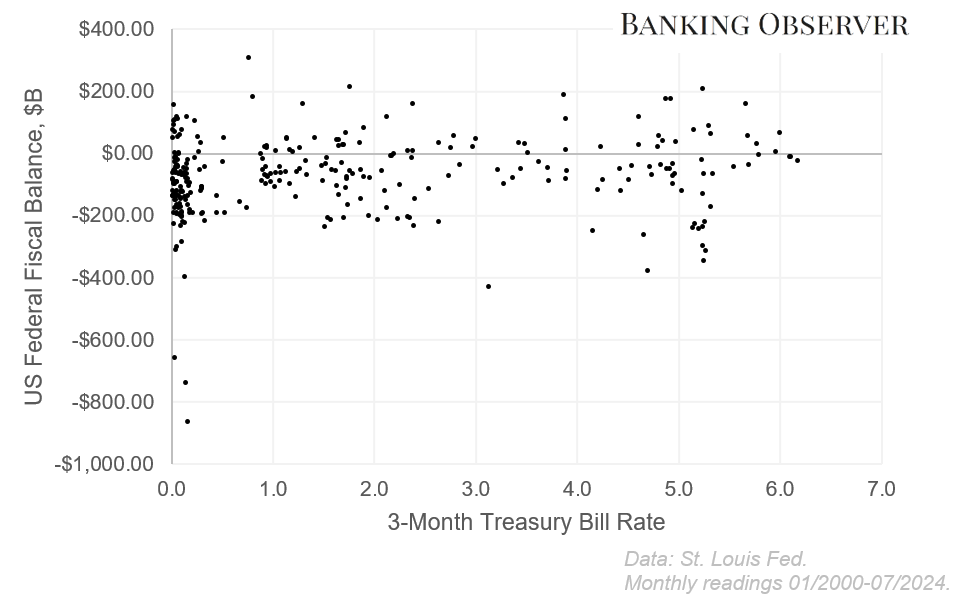

Sounds plausible - but this isn’t how things work in practice. The most obvious reason why is that the Fed sets interest rates as a tool of monetary policy. But the fact that banks can make loans without needing deposits first means that there isn’t a fixed pool of investor money to compete over in the first place.

Unsurprisingly, there doesn’t appear to be any evidence that government deficits push up interest rates.

Data: St. Louis Fed 1, 2

In conclusion…

The main point here is that traditional notions of fiscal responsibility and prudence are misplaced when it comes to the government budget. Deficits don’t have the same impact for currency issuers as they do for households and individuals.

And once we move past artificial constraints like the deficit, we can better understand the true constraints of government spending - namely, inflation. In addition, we can focus on fiscal policy that actually improves real outcomes, rather than policy that tries to balance an imaginary checkbook.

Like this article? Vehemently disagree? Did I miss something? Reply/comment and let me know, I read everything.

Technical note: the US Treasury currently operates ‘as if’ dollars are a limited resource by always maintaining a positive balance in the Treasury General Account, achieved by issuing debt in the open market. But this is a policy choice, not a law of nature, and will be the subject of a more thorough examination in the future - stay tuned.