Is Credit Suisse in trouble?

Probably not, but a lack of confidence could lead to a bank run.

Nassim Taleb, an author and former trader known for betting big on blowups, suggests that when evaluating the veracity of gossip, all rumors should be considered false until officially denied. It might cause some concern, then, that amid swirling doubts about the bank’s health, Credit Suisse CEO Ulrich Körner issued a statement Friday emphasizing the bank’s capital strength and liquidity. Worse, Credit Suisse executives reportedly spent the weekend working the phones, reassuring clients and investors of the bank’s soundness. After a disconcerting year that saw the embattled Swiss bank continue to accumulate losses on a string of debacles, concerns about the storied firm are mounting.

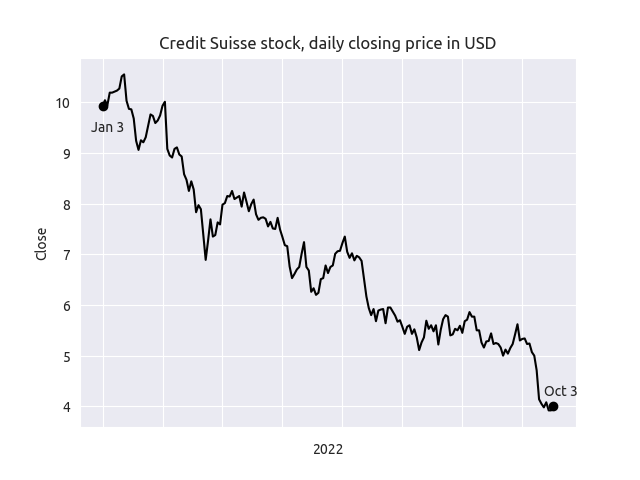

Investor sentiment on Credit Suisse soured after the price of derivatives linked to the bank’s performance began to flash warning signs. Spreads on credit default swaps (CDS), which pay off in the event that the underlying company defaults, climbed to their highest level since 2008. The expected volatility of the firm’s equity, as measured by the pricing of options on the stock, indicated that traders are bracing for an explosive move. The falling equity price has done little to assuage fears. Credit Suisse’s stock price has declined by more than 50% since the start of the year, raising concerns about the bank’s ability to raise fresh capital if trouble brews.

Investors should take note, though, of the difference between a growing risk level and a high risk level. Although spreads on the CDS have increased on a relative basis, they are still low on an absolute basis. Bloomberg columnist Matt Levine noted that with a realistic recovery assumption in the event of bankruptcy, the market implied one-year default risk is still less than 5%. CDS spreads for many investment banks have been rising, indicating gloomy investor sentiment on the financial sector as a whole. Moreover, while options pricing can sometimes portend future volatility, a surge in retail demand for derivatives can muddy the explanatory power of price changes.

Of particular concern to commentators has been the Credit Suisse derivatives book. According to the bank’s 2021 annual report, Credit Suisse has a notional exposure to over $14 trillion of derivative instruments. This astronomical number, paired with the role derivatives played in causing the 2008 crisis, has led to prognostications about the bank triggering a new financial meltdown. But notional exposure is a very poor way to measure risk exposure. A derivative with a notional value of $100 billion could move by several billion dollars each day, or several million, depending on the specific contract. Additionally, many of the derivatives will be held for hedging purposes, which means that losses tend to be offset by corresponding gains.

The 2008 crisis was not an unavoidable consequence of using derivatives, but the result of specific underlying assets not being as safe as many investors assumed. Absent a coherent narrative tied to an actual derivative instrument, it makes little sense to point to the size of Credit Suisse’s book and assume a disaster is inevitable. The advances that have been made since 2008 in ensuring derivatives are centrally-cleared and subject to daily variation margin further reduces the risk of blowup.

The clouds began to clear on Tuesday, as Credit Suisse CDS spreads declined slightly and the stock price popped more than 10% in trading. But the bank, like much of the financial sector, still has an Odyssean journey ahead in navigating a contractionary environment. Higher rates can increase bank profitability, but a recession would slow dealmaking and slash client wealth. Numerous high-profile failures (including Archegos, Greensill, and Citrix) have also raised questions about management competency.

Ultimately, the biggest risk to Credit Suisse is that the sudden lack of confidence, whether justified or not, leads to a bank run. Lenders who choose to pare back short-term funding to the bank can, in aggregate, deprive Credit Suisse of the cash needed to finance its daily operations. Paradoxically, almost any action the bank takes to shore up its liquidity position and prove its strength risks undermining it. Investors will wonder why a healthy bank needs to prove its health.

Despite market rumors, Credit Suisse does not seem to be on the brink of collapse. But it is the nature of financial crises that they are unexpected. Few investors and even fewer government officials saw the 2008 crisis brewing, and it is entirely possible that the market will look back at the Credit Suisse concerns as the first sign that something was broken. If the bank is the first domino to fall, it can expect healthy support from both American and Swiss financial authorities. The bank is a Swiss national champion that is deemed to have global systemic importance.

In the long-term, Credit Suisse’s mismanagement will continue to hamper its growth prospects. The firm’s investment banking and asset management divisions, which are capital intensive and mired in scandal, weigh down a stellar wealth management and private banking operation. Executives have explored spinning off the underperforming arms of the company, perhaps under a revived First Boston brand. The market has not killed Credit Suisse yet, but it may have to shed some dead weight to survive.