The False Premise of the Mar-a-Lago Accord

Don't blame the dollar for America's manufacturing decline.

In an effort to find a coherent rationale underlying Trump’s tariff policy, Wall Street has sought intellectual refuge in the so-called ‘Mar-a-Lago Accord.’ Although Trump has not publicly acknowledged the plan, the Accord is associated with Stephen Miran, one of Trump’s chief economic advisers. In a 41-page paper late last year, Miran laid out the foundations of the Accord, describing the tools America can use to correct a fundamentally unfair global trading system.

In Miran’s telling, the US dollar is persistently overvalued due to the dollar’s status as global reserve currency. In short, because everyone wants dollars to trade and save, the dollar’s value is artificially elevated. Since a stronger dollar makes imports cheaper for US consumers, Miran argues that this overvaluation handicaps domestic manufacturers, leading to job losses, blighted communities, and “deep unhappiness with the prevailing economic order.”

The Mar-a-Lago Accord is a proposal to reverse this status quo. Essentially, Miran’s paper describes the use of tariff threats and security guarantees to pressure countries to deliberately devalue the dollar.1 A new American sovereign wealth fund could also be part of this scheme, purchasing foreign currencies on the open market to depreciate the dollar.

Most popular commentary on the Mar-a-Lago Accord has focused on how dollar devaluation might be achieved, what the financial market impact could be, and how seriously the Trump administration takes this plan.2 But today, I want to step back and critique the Accord’s underlying rationale. In my view, it’s not at all clear that the dollar is to blame for the loss of US manufacturing competitiveness, nor that the dollar is artificially overvalued as a result of global reserve status.

Don’t Blame the Dollar

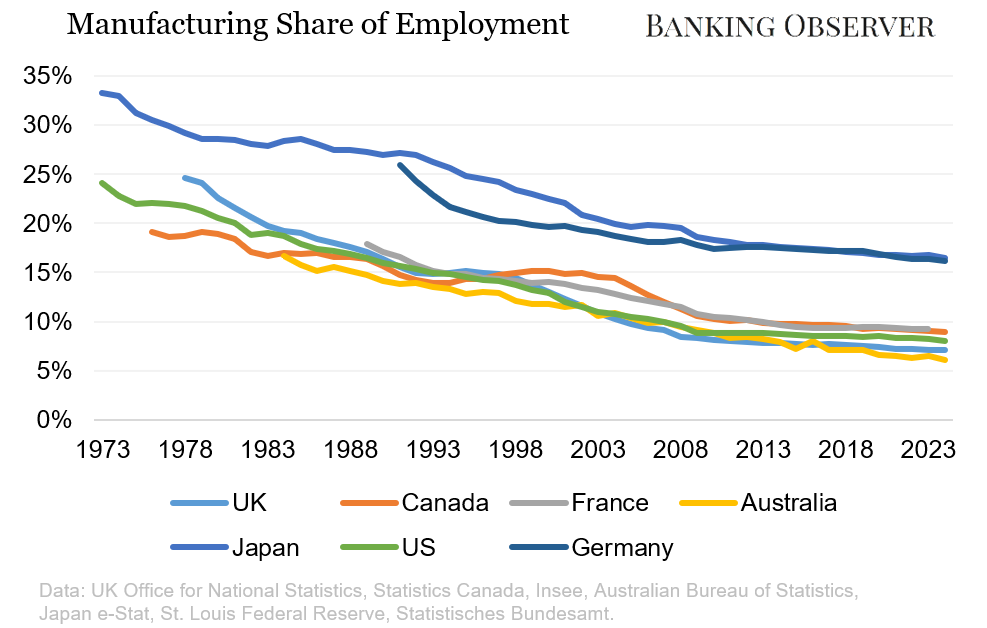

Miran’s thesis is that the dollar’s overvaluation is squarely to blame for the decline of US manufacturing competitiveness and subsequent job losses. If it were truly the case that the dollar is a unique burden on the US, we might expect to see America’s manufacturing base deteriorate quicker or more severely than countries whose currencies are not the global reserve. But this isn’t what the data shows.

Since the 1970s, the manufacturing industry’s share of total employment in America has declined in lockstep with the rest of the rich world. Visually, America’s path is nearly indistinguishable from countries like Australia, Canada, France, and the UK. While countries like Japan and Germany maintain a higher overall manufacturing share, their proportional decline is about the same as the rest of the group.

This data puts paid to the notion that the dollar is a special factor undermining American manufacturing. America’s factories have been hollowed out by the same shifts driving an identical trend across wealthy nations: increasing automation requiring fewer workers, an economy-wide shift toward services, and rising living standards making labor costs less competitive in a globalized market. Despite the dollar’s global dominance, America’s experience hasn’t been unique in this regard.

Is the Dollar Really Overvalued?

The fact that America hasn’t grappled with a uniquely uncompetitive manufacturing industry raises an obvious question: Is the dollar actually overvalued as a result of its reserve status? Miran’s argument seems to take this matter as a point of faith, without demonstrating or proving it. The notion that international demand for the dollar artificially inflates the currency’s valuation seems intuitive and obvious — but that doesn’t mean it’s actually true.

Admittedly, it’s nearly impossible to determine whether or not a currency is truly misvalued. Doing so requires establishing the underlying ‘fair value’ that the current exchange rate deviates from. Since there are many different schools of thought on the correct way to determine this fair value, what is misvalued under one model may be appropriate in another.

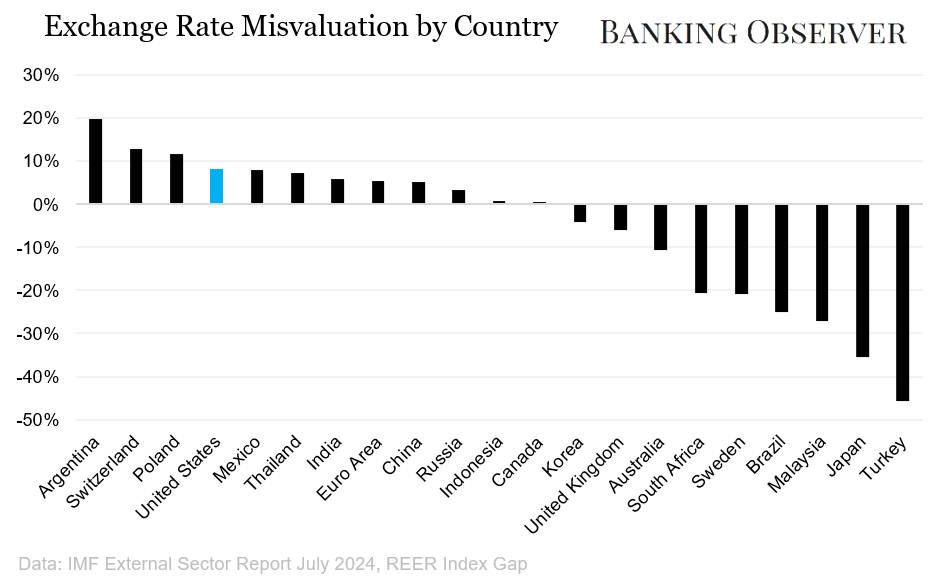

One approach adopted by the IMF is to look at the exchange rate adjustment necessary to bring a country’s current account (typically dominated by imports and exports) into balance over the medium term. ‘Balance’ doesn’t necessarily mean zero, but rather the current account level deemed desirable or appropriate by IMF staff based on factors like demographics, economic growth, and fiscal policy. Flawed as such an approach may be, it provides at least one unified framework for comparing relative currency valuations against each other.

How does the US measure up? As of the IMF’s 2023 assessment, the dollar does appear overvalued, but not grossly so. In fact, the US is sandwiched between Poland and Mexico, whose currencies are similarly overvalued. Suffice to say, neither the złoty nor the peso is being driven higher by reserve currency demand.

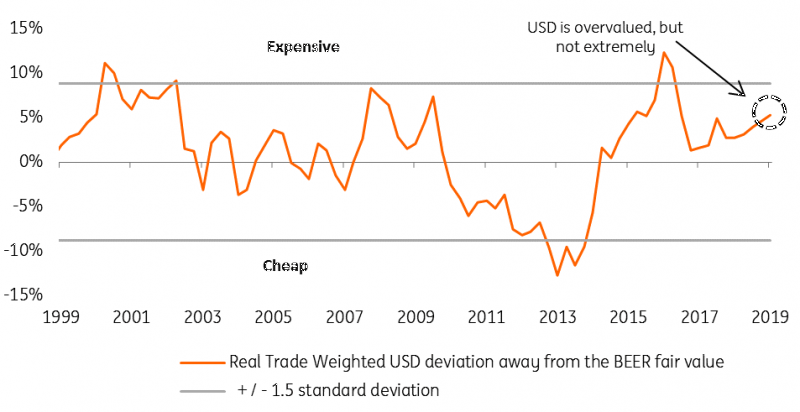

Another related approach, often preferred by Wall Street, is to estimate what a currency’s value ‘should’ be based on historical data relationships with variables like trade and productivity. Dutch bank ING produces a regular series of articles based on this Behavioral Equilibrium Exchange Rate (BEER) approach. Over the past few decades, ING’s estimates show that the dollar’s trade-weighted valuation has consistently traded both above and below its fair value — certainly not evidence of structural overvaluation.

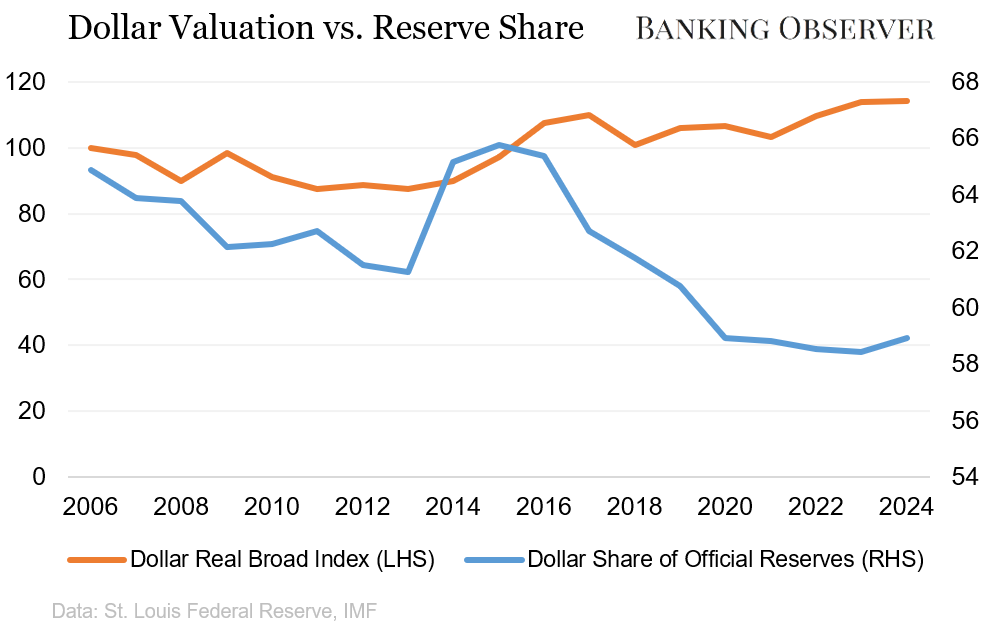

Finally, it’s helpful to look at the relationship (or lack thereof) between the dollar’s reserve dominance and its foreign exchange valuation. Since 2006, the dollar’s share of global official foreign exchange reserves has fallen by about 6 points, reflecting marginally less dollar dominance. Yet over that time period, the dollar’s real trade-weighted valuation (as measured by the Fed’s real broad index) has climbed by 14 points.

The above chart comes with a number of sharp caveats. For one, official global reserves don’t include those held by private savers and corporations. For another, any dollar decline stemming from less reserve dominance could have been overshadowed by factors driving appreciation. However, this chart should make us question the notion that there’s a simple one-to-one relationship between reserve status and overvaluation.

What exactly should we make of all this? On balance, I don’t think there’s sufficient evidence to reject the idea that the dollar’s value may be somewhat distorted by serving as the world’s reserve currency. However, neither is there sufficient evidence of the type of structural, persistent, and unique overvaluation that the Mar-a-Lago Accord posits.

Explaining the Dollar’s Value

On the face of it, this seems like an absurd conclusion. Despite ceding ground to the euro in recent decades, the dollar remains the dominant global reserve currency: nearly 60% of global FX reserves are in dollar-denominated assets, an estimated half of all cross-border payments are in dollars, and the dollar is involved in almost 90% of FX transactions. How could it be possible for all this demand to not severely distort the dollar’s value?

In this section, I want to briefly sketch out an explanation for why the dollar’s reserve status may not necessarily imply structural overvaluation. Note that this argument shouldn’t be taken as a dogmatic conclusion, and I hope to flesh out the details in a future article.

Elastic dollar supply: How markets make dollars

Commentary on how reserve status distorts the dollar’s value typically focuses on the role of global dollar demand. But there is often remarkably little discussion of global dollar supply. In theory, excess dollar demand should only drive up the currency’s value if dollar supply is unable to keep up.

The dollar’s value is ultimately determined in the foreign exchange market, where participants buy and sell different currencies against each other. Crucially, foreign exchange trades settle through currency-denominated bank deposits. Although we might talk about buying and selling abstract ‘dollars,’ what FX market participants are really trading is dollar bank deposits.

Why does this matter? Precisely because bank deposits are not supply-constrained in the way that physical products like oil or grain are. In fact, banks (who play the role of ‘dealers’ in the FX market) can create deposits out of thin air by expanding their balance sheets. When a buyer on the FX market demands dollars, the dealer doesn’t necessarily need to find an offsetting supplier of dollar deposits to close the transaction. Rather, the dealer can simply create new dollars by expanding their balance sheet.3

In a 2013 paper, economist Perry Mehrling provides an example of how this might work in practice. In this telling, an importing country faces a shortage of dollars to settle their payments for international trade. The importer therefore turns to an FX dealer, providing local currency and receiving newly created dollars at the current exchange rate. The importer then transfers this freshly printed deposit to the exporting country to settle the trade payment.

Of course, dealers cannot expand their balance sheets endlessly. Constraints include regulation, hedging risks on the dealer’s new FX asset, and the need to settle outbound deposit transfers (Mehrling’s so-called ‘survival constraint’).4 The essential element to observe, however, is that the monetary system is capable of creating new dollar supply to satisfy excess demand — raising prices is not the only option.

Conclusion: Two Roads Diverged

To recap, the Mar-a-Lago Accord holds that the dollar is overvalued as a result of its reserve currency status and that this distortion has been the key driver decimating America’s manufacturing sector. Based on fundamental valuation models of the dollar and America’s comparative experience with other countries, however, there is little evidence to support these claims. One potential explanation as to why the dollar is not overvalued is the financial system’s ability to create money, resulting in elastic dollar supply.

In other words, don’t blame the dollar for America’s manufacturing decline. Whether or not the Mar-a-Lago Accord is truly behind Trump’s tariffs, the plan isn’t justified in its own right. Trashing the global dollar system won’t bring back America’s industrial capacity because it never destroyed it in the first place.

This isn’t to say that the government doesn’t have the capability to revitalize American manufacturing. As a monetary sovereign, anything that America can do, America can afford. But since taking the public spending road would involve greater deficits, higher government debt, and increased state intervention in the economy, don’t hold your breath waiting for the Trump administration to do so.

The Mar-A-Lago Accord takes its name from the 1985 Plaza Accord, in which the US and four allies agreed to deliberately devalue the dollar.

It seems fairly clear to me that Trump isn’t following the Mar-a-Lago Accord, particularly since withdrawing from global security relationships is at odds with Miran’s plan. Nonetheless, it’s worth understanding the plan to weigh the government’s policy options to reshore manufacturing.

Notably, dealers in the FX market aren’t the only creators of international dollars. The eurodollar market, the shadow banking system, the Fed’s swap lines, and other structures all foster the elasticity of global dollar supply as well. The FX dealer example, however, provides the clearest example of how dollar creation can mitigate currency appreciation.

Settlement constraints deserve their own article, but it’s worth mentioning a few key points.

For US bank dealers with access to the federal funds market, settlement constraints are ultimately profit constraints. If a US bank needs to acquire reserves to settle the outflow of a newly created deposit, it can always do so by borrowing reserves at (approximately) the federal funds rate. If reserve demand climbs too high, pushing the fed funds rate up, the Fed will step in to inject more reserves into the system. Thus, US banks can always settle their obligations for a fairly well-known price.

The Fed’s accommodation of reserve demand also extends, indirectly, to non-US banks. Consider a non-US bank dealer facing an outflow of a newly created dollar deposit. To satisfy settlement, the bank may need to borrow dollar deposits from a US bank, which itself has access to the fed funds market. If offshore banks face settlement stress and need to borrow deposits, onshore banks can profit by lending to them at a high rate and borrowing in the fed funds market to satisfy any settlement of their own.

This analysis is somewhat outdated given that the US banking system currently operates with excess levels of reserves (meaning that the fed funds market is largely dormant) and that offshore dollar markets have largely shifted to secured borrowing (thanks to post-GFC regulations). However, it does offer useful intuition as to why settlement constraints do not undermine the ability of banks to create money through balance sheet expansion.