The FTX collapse can teach us the ABC’s of banking

The first rule of bank club: don’t make levered bets on your own stock.

Despite FTX’s reputation for innovativeness and professionalism, the firm seems to have been taken down by a fairly classic risk management error. When lending money, the value of any collateral should be unrelated to the performance of either the lender or the borrower. Although straying from this principle in either direction isn’t ideal, neither are deviations symmetric. While it’s bad for collateral quality to be correlated to the performance of the borrower, it can be catastrophic for collateral quality to be correlated to the performance of the lender. Although the FTX fallout is likely to be contained to crypto markets, the episode is highly instructive for those in traditional finance.

Suppose a bank lends someone money to buy a house, and the bank’s loan is secured by the value of the home. If the borrower loses their job, and is unable to repay the loan, the bank will just seize the home. Since the value of the collateral (the home) is independent of the credit quality of the borrower, the bank should be able to avoid any losses by selling the house and recouping their investment. If the bank has lent $80 against a home worth $100, the value of the house shouldn’t drop to $70 just because the borrower’s financial situation deteriorated1. Factors that affect the borrower’s credit quality will not affect the collateral quality, making this an ideal lending situation.

Although lending against collateral that is correlated to the borrower is riskier, it’s still viable. Consider the situation of a bank lending money to Elon Musk against the value of his Tesla stock. If Elon were to be arrested, then this would probably 1) make it more difficult for him to repay the loan and 2) cause the value of Tesla stock to collapse. This isn’t great for the bank, since the collateral value would be deteriorating at the same time that it starts to really matter, but it’s manageable with proper precautions. As long as lenders have a low loan-to-value ratio (like only lending $30 against $100 worth of Tesla stock), have suitably liquid collateral (so that the assets can be sold quickly), and charge a high enough interest rate on the loan (to cover potential losses), they shouldn’t lose money even if collateral value is correlated to the performance of the borrower.

Now, what about the situation where collateral value is correlated to the performance of the lender? For a simple example, consider a bank lending money to a client collateralized by the value of its own stock. Bloomberg columnist Matt Levine referred to this as “dark magic”, which feels pretty accurate. If the market becomes concerned about the bank’s health, its stock price will fall, which will cause the value of the collateral to decline, which will make the bank unhealthier, which will cause its stock to fall more, which will cause the value of the collateral to decline, and so on. The spiral dynamics can be vicious. If the bank tries to dump its own stock on the market to arrest this situation, they’re likely to drive the price down even further, with knock-on effects for the bank’s liquidity and solvency.

The more correlated the collateral is to the lender, the worse the dynamics become. Goldman Sachs might be willing to lend to a client collateralized by stock in British American Tobacco, but they probably shouldn’t lend to a client collateralized by stock in Morgan Stanley. If concern spreads about the health of all investment banks, Morgan Stanley stock will fall, which will cause the collateral value to deteriorate, which will cause Goldman stock to fall, which might spark more concern about investment banks, which feeds back into Morgan Stanley stock, and so on. In the case of FTX, the collateral wasn’t perfectly correlated with the health of the firm as a whole, but it was correlated enough to trigger these spiral dynamics.

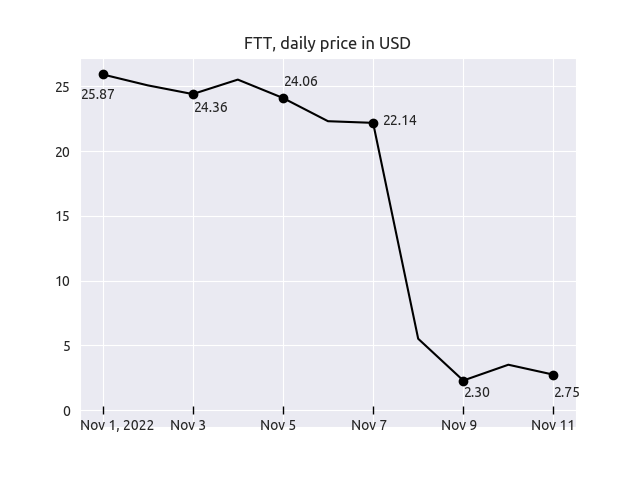

The full story of the FTX debacle won’t be known until the dust settles and the lawyers disperse, but reporting by CoinDesk and Bloomberg helps confirm the theory that FTX’s key mistake lay with poor collateral management. Roughly, FTX lent huge sums of money to associated hedge fund Alameda Research2 to conduct leveraged trading3, and accepted FTX’s native token FTT as collateral. Although FTT isn’t exactly stock in FTX, it can be thought of as stock-lite, with mechanical features that should make it rise and fall in accordance with FTX’s popularity and profitability4. After concerns about FTX spread (in part caused by tweets from a rival CEO), the value of FTT started to fall, triggering a spiral. The decline in price of FTT left FTX’s loans undercollateralized, which caused a further collapse in FTT’s price, and left a growing hole in FTX’s balance sheet5. Thin volume and concerns about knock-on effects would have limited FTX’s ability to sell their FTT collateral.

Ideally, collateral should be a stable, independent asset, like cash or government bonds. With proper precautions, lenders can accept collateral with a value related to the credit quality of the borrower. But lending against collateral correlated to the quality of the lender can easily trigger a spiral that destroys a company. In the end, FTX was unable to escape from this spiral, and the firm filed for bankruptcy today. The difficulty with building a new financial system is that you might miss some of the lessons of the old one. In this case, FTX missed a simple rule of banking. Don’t lend against the value of your own stock.

1. This isn’t always true. If an entire town faces an economic decline, causing people to lose their jobs, then home prices will fall as well. This destroyed tons of local banks in the Great Depression whose loan books were made up of geographically concentrated mortgages. Here, we’re referring to one borrower who loses their job due to, like, misconduct, not a regional depression.

2. Sam Bankman-Fried, the (former) billionaire founder of FTX and Alameda, owns (owned?) both companies.

3. This probably sounds risky in itself, but this line of business is actually quite common. In traditional finance, prime brokerage departments at investment banks offer margin to hedge funds. As long as collateral requirements are well managed, the bank shouldn’t run into trouble. When collateral requirements are not well managed, Archegos happens. Margin trading in crypto is often actually safer for the lender, because borrowing is done programmatically and positions are automatically liquidated if collateral is not maintained. That obviously was not the case with Alameda and FTX, which had a relationship closer to the traditional finance end of the spectrum.

4. The FTT token offered discounts for trading with FTX, so the more demand there was for trading on FTX, the more demand for FTT. FTX also had a mechanism to remove FTT from the market, raising its price, with higher trading revenues meaning more FTT was ‘burned’. These mechanics make FTT an approximation of a stock for FTX.

5. This collapse is similar to the dynamics of algorithmic stablecoin death spirals, like Terra/Luna. Convertible bonds can cause similar issues.